Thresholds update 2021

Thresholds for income tax purposes

The limit for 2021 for tax on registered income without deductible costs

Starting from 2021, the right to apply tax on registered income without deductible costs will have the taxpayers who in 2020:

- obtained revenues from sole proprietorship in the amount not exceeding PLN

9,030,600.00 (EUR 2,000,000 × PLN 4.5153/EUR), or

- obtained income exclusively from activities conducted as a civil law partnership

of natural persons or a general partnership of natural persons, provided that the total income of the partners of the partnership from these activities did not exceed PLN 9,030,600.00 (EUR 2,000,000 × PLN 4.5153/EUR).

The right to apply tax on registered income without deductible costs on a quarterly basis will be granted in 2021 to taxpayers whose revenues from business activity conducted independently or revenues of the partnership did not exceed in 2020 the amount of PLN 903,060 (i.e. EUR 200,000 × PLN 4.5153/EUR).

Small taxpayer status

A small taxpayer is a taxpayer whose sales revenue (along with the amount of VAT due) did not exceed in the previous tax year the equivalent of EUR 2,000,000 in Polish zlotys.

In 2021, a small taxpayer shall be a taxpayer whose sales revenue (including the amount of output VAT) does not exceed in 2020 the amount of PLN 9,031,000 (EUR 2,000,000 × PLN 4.5153/EUR, when rounded to PLN 1000).

It is worth mentioning that in 2021 taxpayers holding a small taxpayer status will

be able to:

- pay advances on income tax on a quarterly basis,

- if they are CIT taxpayers, 9% CIT rate shall apply, in case their revenues do not exceed EUR 2,000,000 in a given tax year, (PLN 9,097,000, exchange rate4.5485 PLN/EUR from the first working day of a given tax year),

- recognise one-off impairments

One-off depreciation limit for small taxpayers or entities commencing to trade

Small taxpayers and taxpayers commencing their business activity (in the year of its commencement) are entitled to one-off depreciation of fixed assets classified as group 3-8 KŚT (with the exception of passenger cars). A one-off impairments are being recognised in the tax year in which such assets are entered in a fixed asset register, up to an amount not exceeding the equivalent of EUR 50,000 of the total value of such depreciation write-offs in a tax year. The

limit for one-off impairments write offs in 2021 will be PLN 226,000.

One-off depreciation for all taxpayers in relation to acquisition of new fixed assets.

All taxpayers may benefit from one-off depreciation under the new rules in relation to new fixed assets - groups 3-6 and 8 of KŚT - up to the amount not exceeding PLN 100,000 in a tax year.

One-off impairment on fixed assets acquired for the purpose of manufacture of goods related to the COVID-19 countermeasures.

In 2021, taxpayers will be able to recognise one-off impairment write-offs on the initial value of fixed assets acquired for the manufacture of goods related to COVID-19 countermeasures and entered in the records of fixed assets and intangible assets during the period from 2020 to the end of the month in which the epidemic state declared due to COVID-19 was revoked.

Income thresholds for accounting purposes

Setting the bookkeeping obligation in 2021.

Accounting books must be kept by natural persons, civil law partnerships of natural persons, general partnerships of natural persons and partnerships, if their revenues for the previous tax year (fiscal year according to the Accounting Act) reached at least the equivalent in Polish currency of EUR 2,000,000 (cf. Art. 24a par. 4 of the PIT Act and Art. 2 par. 1 pt. 2 of the Accounting Act). After conversion of the amount of EUR 2,000,000 using the applicable exchange

rate (PLN 4.5153/EUR), this limit will equal PLN 9,030,600.

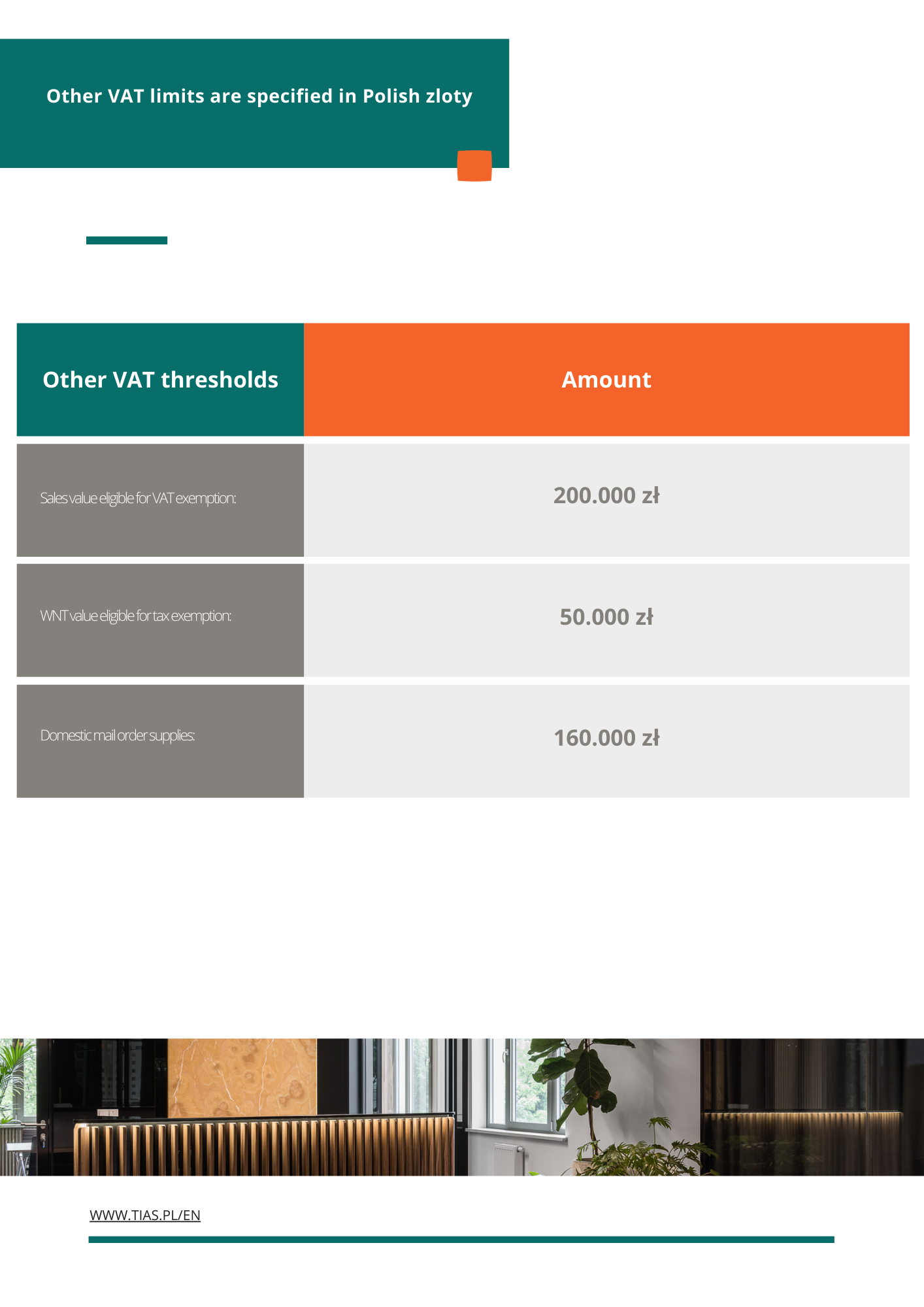

Income thresholds for VAT purposes

Small taxpayer

In 2021, a small taxpayer for VAT purposes shall be a taxpayer whose sales value (together with the tax amount) did not exceed in the previous tax year the PLN equivalent of EUR 1,200,000; this limit for 2021 amounts to PLN 5,418,000 (EUR 1,200,000 × PLN 4.5153/EUR, rounded up to PLN 1,000).

Small taxpayers can benefit from certain simplifications, i.e. they may settle VAT:

1) using a so-called cash method,

2)quarterly

Taxpayers registered by a head of tax office as active VAT taxpayers - for a period of 12 months starting from the month of registration - are not entitled to settle VAT quarterly.

O autorze

Zobacz również

Good migration law as one of the pillars of support for Ukraine

At this turbulent time, as armed conflict still rages on in Ukraine, it is important that we are able to concentrate on prospects of relief and future reconstruction.

.png)

The CbC reporting deadline is drawing closer

As part of the OECD's framework to counter the transferring of profits to tax havens, a Country by Country (CbC) reporting mechanism has been established.

TIAS among the winners of the prestigious „Forbes Diamonds 2024” award!

Z radością i dumą informujemy, że nasza firma została laureatem prestiżowego rankingu „Diamenty Forbesa 2024”!